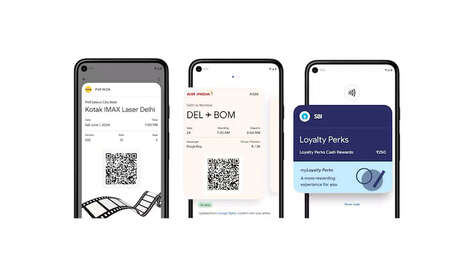

The National Payments Corporation of India (NPCI) has adopted a Unified Payment Interface. This allows customers to use their mobile number in place of bank account details to make a payment over the phone or on the Internet. By simplifying the purchasing path for people, the Unified Payment Interface ensures a user-friendly experience as well as optimal convenience.

A great option for smaller banks that don't have the proper infrastructure to create their own e-wallet, the Unified Payment Interface provides a slew of possibilities. NPCI states, "Whole focus on simplifying payment, idea is to go for largely cashless system. Not changing infra or getting new payment system so we are creating a facility whereby payments products can be launched by banks using imps."

Key Themes Behind This Trend

- Unified Payment Interface

- The introduction of NPCI's Unified Payment Interface has simplified the purchasing path and created possibilities for cashless systems.

- Mobile Payment

- The use of mobile numbers in place of bank account details for payments creates a user-friendly experience and convenience, paving the way for more mobile payment options.

- Simplifying Payment

- The whole focus on simplifying payment creates opportunities for businesses to create innovative solutions that provide a seamless and hassle-free payment experience for customers.

Where This Applies

- Banking

- The Unified Payment Interface has created opportunities for smaller banks to offer e-wallet services without the need for extensive infrastructure investment, enabling them to compete with larger banks.

- Fintech

- The use of mobile numbers as a payment measure opens up opportunities for fintech companies to create new and innovative services that make it easier for people to transact in the digital economy.

- E-commerce

- The Unified Payment Interface streamlines the checkout process, increasing the likelihood that consumers will complete their purchase, which could lead to an increase in e-commerce transactions.